Now 2024 is over and we look forward to 2025, confirming our budgets and strategies for the year ahead. A heavy emphasis has been put on Q4, with good reason—holiday shopping, Black Friday, and Boxing Day Sales make it the busiest and fastest-paced time of the year for marketers, agencies, and retailers.

As we look back on 2024, which became the year of the smarter, more informed shopper—as we covered in our Are you ready for Black Friday Post — consumers made decisions earlier in the year and began planning their holiday shopping as early as May. We did a deep dive into the figures to see how Q4 performed.

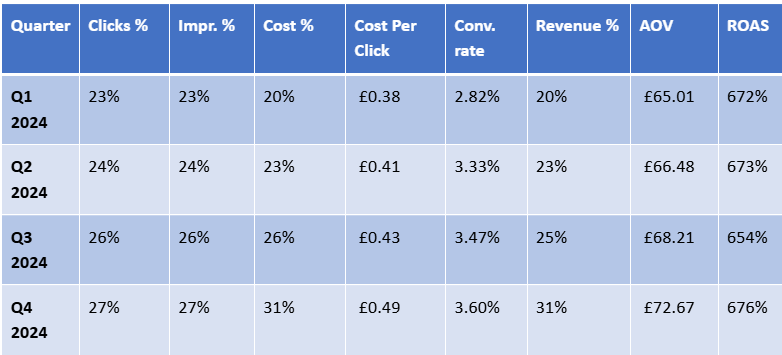

Q4 was the biggest month of the year in both ad spend and revenue generated, with 2024 outspending 2023 by 28%, and generating 30% more revenue for retailers. This shows that advertisers are continuing to spend more to make more year on year, with ROI staying static.

Q4 made up 31% of revenue and ad spend in 2024. Although ad spend and revenue had significant jumps, clicks and impressions saw only a slight increase, making up 27% of 2024. The bulk of the increase was due to a higher Average Order Value (AOV) in Q4 and a significant increase in cost per click (CPC), suggesting that while year-round searches were marginally up, buyer intent was significantly stronger, and the shopping auctions were at their most competitive.

CPCs were at £0.49 in Q4, up 29% from Q1, which resulted in ROAS staying fairly in line with the yearly average. Although more revenue was generated in Q4, the cost of a click brought profit levels down. CPCs were up 23% from 2023, so although CPCs came down in Q1, by Q2, they were already above the 2023 Q4 levels.

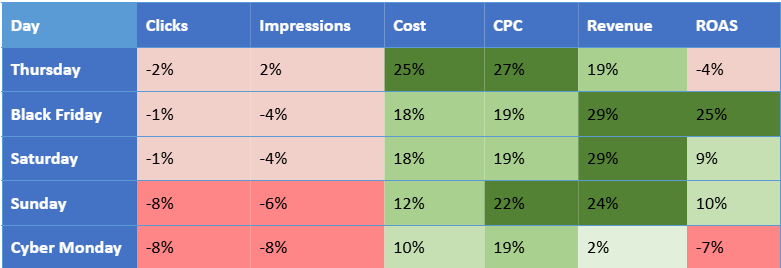

The most anticipated period of Q4 is the Black Friday weekend, with shoppers becoming increasingly savvy about saving their holiday shopping for the biggest sales of the year. Black Friday was significantly the biggest day of the year, with retailers generating 38% more revenue than any other day outside of the Black Friday weekend, which includes Thanksgiving. We also saw Black Friday spending 28% more than any other day in 2024.

ROAS saw huge spikes, with Performance Max campaigns coming in at 780%, and Shopping Ads in Performance Max hitting 812%. For those running manual shopping campaigns, ROAS reached 930%, with the use of manual shopping campaigns doubling year-on-year, though these campaigns only accounted for 7% of overall shopping spend.

Year-on-year ROAS for the 10,000 campaigns we analyzed showed a 25% increase in ROAS. Although clicks and impressions were marginally down over the entire period, Black Friday was a roaring success for most advertisers. However, there were some notable trends this year. Last year, Cyber Monday was second to Black Friday in terms of revenue. This year, Sunday of the Black Friday weekend claimed that crown, while Cyber Monday saw a 7% dip in ROAS. The Sunday of the weekend saw an 8% increase in revenue compared to Cyber Monday, while in 2023, this figure showed an 11% dip.

While Cyber Monday remains a key sales event, its success largely depends on the retailer's deals. If a sale is exclusive to Black Friday and continues through the weekend, it might be better to shift the budget focus toward Sunday. However, demand remains strong on Cyber Monday, with shoppers still seeking fresh deals, so depending on your promotions, there could still be opportunities on Cyber Monday.

Although Black Friday remains the major day, revenue and spend began to pick up heavily on Thanksgiving, with the five-day period being the top revenue and spend-generating day, as it was last year.

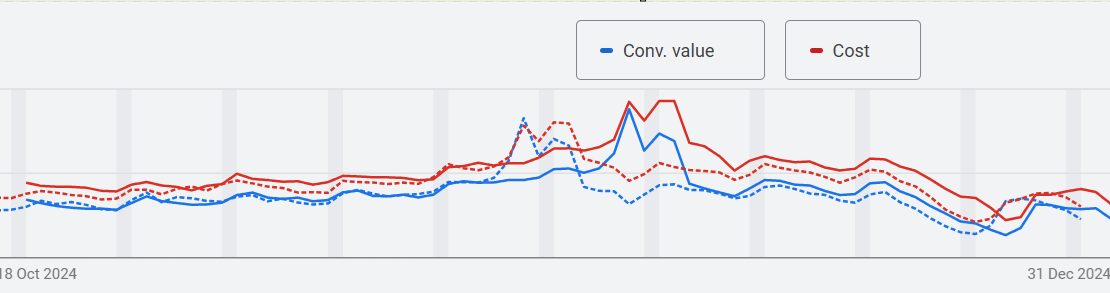

One significant difference in 2024 was that Black Friday occurred five days later in the year, bringing it closer to Christmas. 2025 will follow the same pattern. This created a longer build-up to Black Friday, with costs and revenue beginning to gradually pick up from October 20th, peaking on Black Friday weekend before remaining steady until the last Wednesday before Christmas.

Strong Line 2024 Data

Dotted Line 2023 Data

After Cyber Monday, there was a clear drop-off in spend and revenue, with a 26% drop in spend and a 36% drop in revenue leading to a 13% decrease in ROAS the following day. Identical drops were observed in 2023. Tuesday through Thursday saw a dip in ROAS, with those three days making up three of the six lowest ROAS days during the period, along with December 22nd, 23rd, and 24th. Advertisers will need to manage their budgets more carefully after Black Friday. Although ROAS was 5% below average, there was a 26% drop in ROAS from Black Friday to the following day.

After navigating through the Black Friday weekend and the subsequent week, the following week was steady, with the two remaining weekends before Christmas showing the biggest peaks in performance, particularly on Sunday. From there, Q4 began to wind down with Christmas Eve and Christmas Day being the two lowest-spending days of the year, with Christmas Eve being the lowest revenue day of the year—making 19% less than December 23rd, the second-lowest revenue day of the year.

Christmas Day, however, showed strong ROAS performance at 718%, 10% higher than the yearly average, as the traditional in-store Boxing Day sales are now launched on Christmas Day (or earlier), allowing consumers to pick up bargains on gifts they may have wanted for Christmas but didn’t receive.

The sales then picked up on Boxing Day, which was the biggest sale day of the year in Britain up until 2014, when Black Friday took over. Retailers now spend 2.5 times more on Black Friday than on Boxing Day.

Boxing Day and the following day showed strong performance, with a ROAS of 856%, making it the most profitable day of Q4. From there, although spending picked up on December 27th with a strong ROAS of 730%, performance began to slow. This could be due to advertisers reacting to the performance of the previous few days.

Although Clothing & Accessories generated the most revenue year-on-year in Q4, there was only a 4% increase in revenue through Google Shopping, although the overall increase in Google Shopping was 19%.

The biggest gains came from Home and Garden, which increased by 67%, driven by Beds & Accessories (+88%) and Lighting (+77%). Health and Beauty also saw a 65% year-on-year increase, although Cosmetics were down by 22%. Fitness and Nutrition grew by 150%.

One of the biggest standout revenue drops came from Books, which saw a 50% year-on-year decline, possibly indicating a shift toward audiobooks.

Overall, Q4 was a huge success, but to make the most of 2025, advertisers need to be highly prepared for budget management. We have compiled the following takeaways to ensure success in 2025:

Monthly Subscription

April 22, 2025

February 6, 2025

November 7, 2024

October 22, 2024

December 19, 2023